DAVIS KEDROSKY – MARCH 30TH, 2020

EDITOR: AMANDA YAO

Interest rates are weird. How weird? Well, yields on ten-year treasury notes are at all-time lows and plunging toward zero, and equivalent sovereign debt remains negative across Europe. Wall Street commentators are warning of rate-related perils, from housing market distortions and eroded retirement savings to crumbling bank profitability and excessive borrowing. Worse yet, rates near zero inhibit central banks’ ability to respond to a recession, which now appears to be imminent. Economic growth is slow, at least in historical terms—and even inflation, which normally rises in response to low rates, is sluggish. In short, monetary policy and the money market can hardly be more expansionary, but no expansion—except for consumer and public debt—has materialized.

The prolonged recovery of the world economy in the wake of the global financial crisis is an oft-mooted cause. Treasury yields, or the price charged to the government on each borrowed dollar, have not reached previous levels after halving from 4% to 2% in late 2008. Some attribute low yields to widespread difficulties in boosting growth and inflation in a reviving economy. Efforts by the Federal Reserve, whose responsibility is to set short-term nominal rates and to lift the federal funds rate away from the zero lower bound—literally of 0%, a point beyond which American yields had never descended—have been lately scotched. After a series of gradual raises starting in 2016, the Fed has cut interest rates three times in just the last year in the face of recession threats. In Europe, where the post-recession path to renewal wound through deflation and debt crisis, the European Central Bank set rates negative in 2014 and is currently reinstating quantitative easing. Something broke in Western economies a decade ago, the above theory goes, and efforts to reinstate “normal” conditions are now effectively contractionary policy. Combine that with increasing investor fears about the present state of the business cycle—and, of course, about global political stability, behind the latest drop in 10-year yields—and the explanation seems complete.

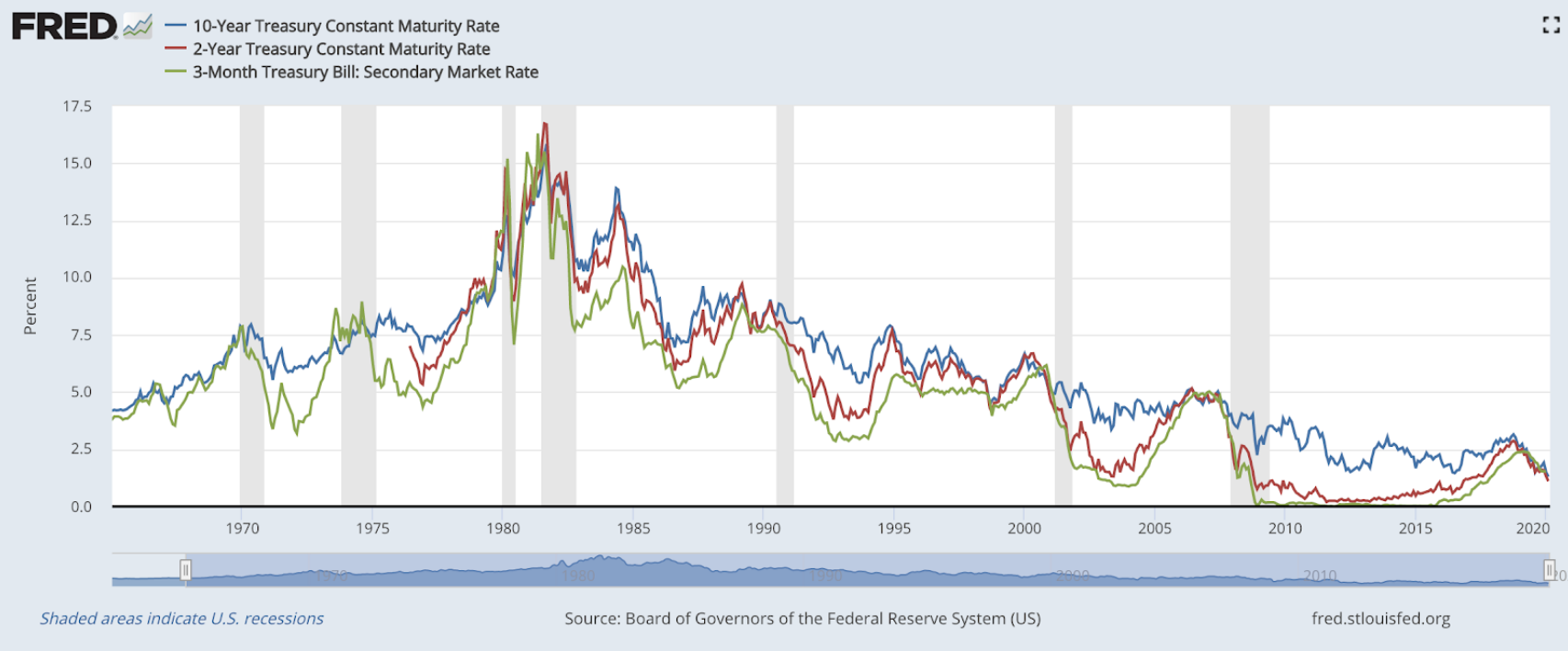

A glance at the longer trajectory of American interest rates invites skepticism. After climbing to a historic peak of 15.84% in September 1981 during the so-called Volcker disinflation, the 10-year Treasury rate has trended downward ever since. Indeed, the drop in 2008 looks insignificant from this broader vantage point, appearing to be a momentary acceleration of a deeper historical process. Although the 2-year and 3-month bills display greater volatility, they follow the same track.

Even once inflation is factored in to produce the safe real interest rate, a steady decline after the Volcker era is clearly visible. This indicates that something fundamental is changing in the economy’s view of saving and investment. Bloomberg pundit Joe Weisenthal has glibly suggested, echoing views common on Wall Street, that sovereign bonds—indeed, a wide range of financial assets—are actually stores of value and that negative rates are fees for safehousing money. He cites the purported use of medieval castles and art as assets, both of which were expensive to maintain. Leaving historical accuracy aside, however, each did provide owners with direct utility, the former as a defense mechanism and the latter as a prestige good with aesthetic merit.

Furthermore, Weisenthal ignores the historic functions of debt and interest: to allow borrowers to smooth their consumption over time or fund large projects and to compensate for default risk. A US bankruptcy may be unlikely, but in Europe, just half a decade removed from the Greek debt crisis, the notion that states are immune to insolvency is laughable. At best, the present security of the American regime is a reflection of path-dependent geopolitical and financial circumstances (as the creator and chief backer of the post-World War II economic order), not of the fiscal status of the modern nation-state in general. Indeed, the belief that America is a risk-free borrower may invite enough leverage to produce higher default risk.

Among academics, Harvard economist Lawrence Summers has revived the time-honored threat of secular stagnation, or “a chronic tendency of private investment to be insufficient to absorb private saving [that] leads, in the absence of extraordinary policies, to extremely low interest rates, inflation that is lower than desirable, and sluggish economic growth.” This disparity has driven down the “private sector neutral real rate”—where savings and investment meet—by 700 basis points since the 1970s despite the twin explosions of the American welfare state (via pensions, healthcare provision, and other transfers) and of public debt, both of which have propped up borrowing costs by 3.5 to 4 percentage points. Moreover, Summers believes that the phenomenon is global, linked to demographic and structural factors operating across the developed world for decades. These include aging societies (due to the simultaneous decline of population growth and rise of life expectancy worldwide), deglobalization, wealth inequality, and a marked decline in productivity growth. The combination of increased saving for prolonged retirements with lowered expectations for American economic prospects, at least in standard macroeconomic models, could have created the pool of excess investment supply. An October 2019 paper in The American Economic Journal: Macroeconomics disputes the influence of expectations, specifically with regard to inequality and productivity, but confirms that safe real interest rates are negatively correlated with the proportion of the population aged 40-64 and positively correlated with hours worked. With a greater percentage of households reserving cash for lengthier retirements, interest rates will inevitably be depressed. The United States, as Summers argues, may become Japan—perpetually reliant on fiscal stimulus for continued growth, however creaky.

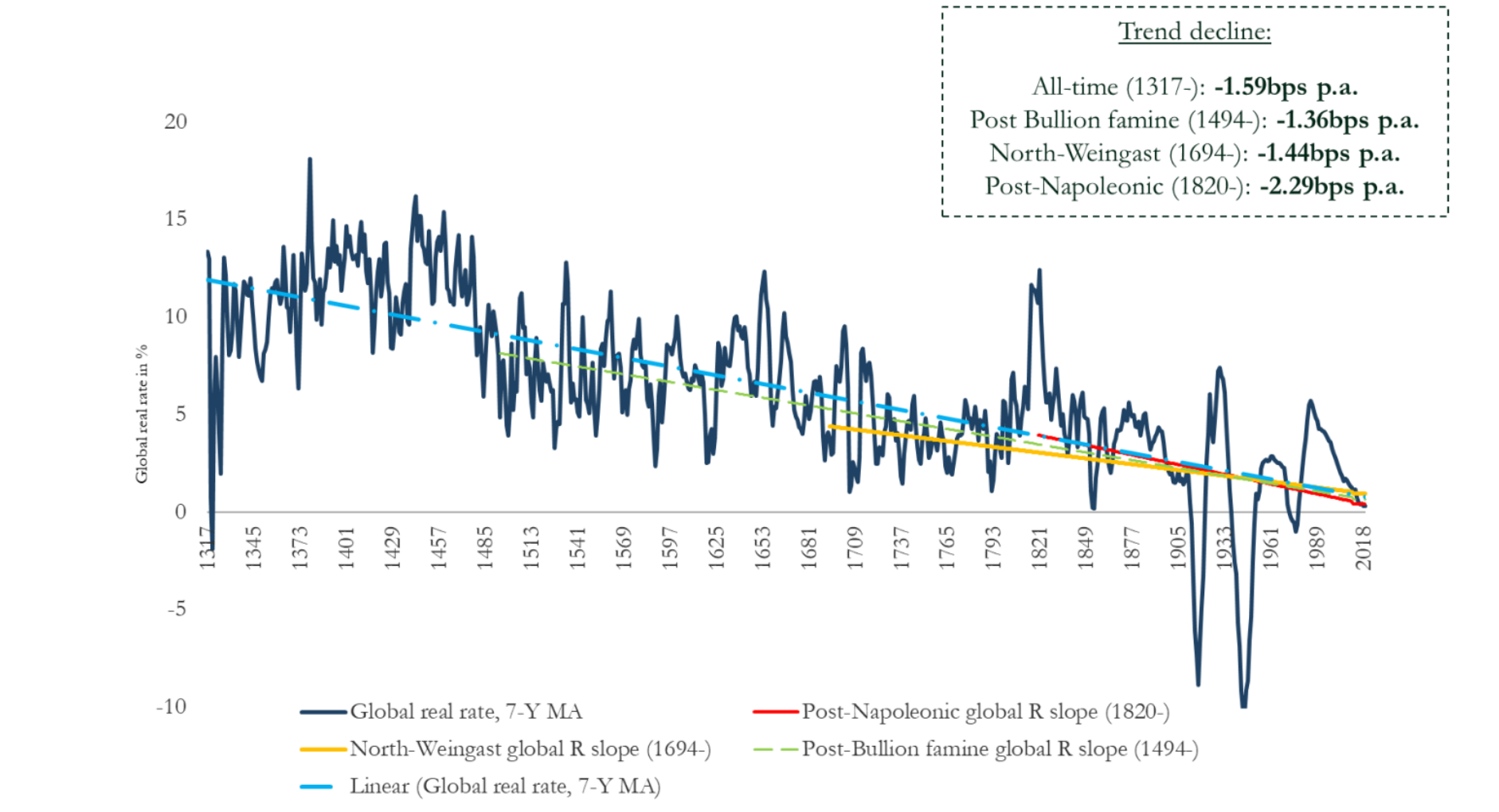

Image Source: Schmelzing 2020

As Harvard’s Paul Schmelzing wrote in a January paper, a longer-term look might be warranted. After cataloguing returns on safe assets for the previous 707 years, Schmelzing found, somewhat astonishingly, that “global real rates have shown a persistent downward trend over the past five centuries, declining within a corridor of between -0.9 and -1.75 basis points per annum.” Since the Black Death, in short, real interest rates or their equivalents have been plunging inexorably toward zero—a “suprasecular” stagnation. The causes of this slide, Schmelzing admits, must remain unclear, given the fragility of the archival dataset. However, he speculates that a combination of general capital accumulation after the Black Death—a negative population shock that raised wages and consumption, leading monarchs to enforce prudence—and the transition of state governments toward constant service provision might have played a role. When incomes grew, workers increased their surplus incomes (everything unnecessary for subsistence), allowing them to save in often exclusive European banks. Other potential explanations include rising life expectancies and shorter, less destructive conflicts, but he sees no correlation between periods of peace and trend decline.

One upshot, for Schmelzing, is that “the ‘secular stagnation’ narrative, to the extent that it posits an aberration of longer-term dynamics over recent decades, appears fully misleading”—overemphasizing a return to the ancient trend line. He predicts that short-term rates will become permanently negative within the decade, as will long-term rates (higher for the greater implied risk) sometime after 2050. Returns have been negative on 46 occasions since 1311, when the series began; of these, 29 came after 1900, with no instances prior to the seventeenth century. Schmelzing also argues that volatility, or the standard deviation from the real rate, has also been falling, suggesting a more predictably negative future. The sorts of monetary and fiscal interventions—public spending, negative nominal rates, and supply-side structural reforms—floated by Summers and others as permanent solutions may only produce temporary effects at colossal expense.

No single paper should be taken as gospel, especially one reliant on (necessarily) unreliable pre-modern data. Indeed, the evolution of financial systems during the last century may have transformed capital markets such that present patterns are anachronistic when applied to sixteenth-century counterparts. The Wall Street of quantitative hedge funds, derivatives, and indexing bears only a superficial resemblance to sixteenth-century Augsburg. Returning once again to recent decades, colossal deviations from trend are obvious, and can be conclusively related to shorter-term economic events—interest rates tumbling during the Great Depression and rising again amid the military spending drives of World War II, for example. Old forces can be easily subordinated to the new.

One compelling explanation for falling interest rates since 1980 is the worrying decline in output growth over the last four decades. Economist Robert Gordon, in his 2014 bestseller The Rise and Fall of American Growth, argues that growth in total factor productivity (TFP), a common measure of output efficiency, has slowed since 1970, stalled by a combination of demographic pressures, poor human capital investment, and technological stagnation. Annual TFP growth fell from 1.89% over the period 1920 to 1970 to just 0.57% over the next twenty years, and improved rates of 1.03% during the internet boom soon gave way to a dismal 0.4% through the early 2000s. Surprisingly, Gordon hypothesizes that the cause is chiefly technological: “the pace of innovation since 1970 has not been as broad or as deep as that spurred by the inventions of the special century (1870 to 1970),” and occurred “narrowly” in an “evolutionary and continuous” manner.

Immersed in anxieties about automation, surveillance, and alienation, Gordon’s view can seem absurd. But powerful confirmation comes from the natural sciences, where discoveries across a range of disciplines, from physics to neuroscience, have been wrested slower than expected, demanding unprecedented levels of funding and manpower. As early as 2007, surveys found that team-based research was becoming more prevalent in essentially all science and engineering fields, especially among high-impact papers. This trend has strengthened continuously ever since. In short, scientific innovation—inextricably linked with technological progress—is probably becoming more difficult, and at the very least, more expensive. Whether the intractability is due to a profligate government-led model, as Terence Kealey famously claimed, or to something inherent to knowledge itself is uncertain. What is obvious, however, is that the resulting paucity of investment prospects would decrease demand for the swelling pool of surplus capital, lowering interest rates. Money is cheap because it is less obvious what can productively be done with it.

Whatever the cause, the present depression of real interest rates is unlikely to be merely cyclical. The American economy is no longer the vigorous behemoth of the postwar years, fueled by generous infusions of young, ambitious workers and technological novelties. Instead, the developed world—to which America is no exception—seems to be converging on the Japanese paradigm of societal aging, constant stimulus, and absent growth. Unless something dramatic changes, major indicators will eventually come to reflect that fact.

Featured Image Source: New York Times

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the Undergraduate Economics Association, the UC Berkeley Economics Department and faculty, or the University of California, Berkeley in general.