SETH BERTOLUCCI – DECEMBER 15, 2018

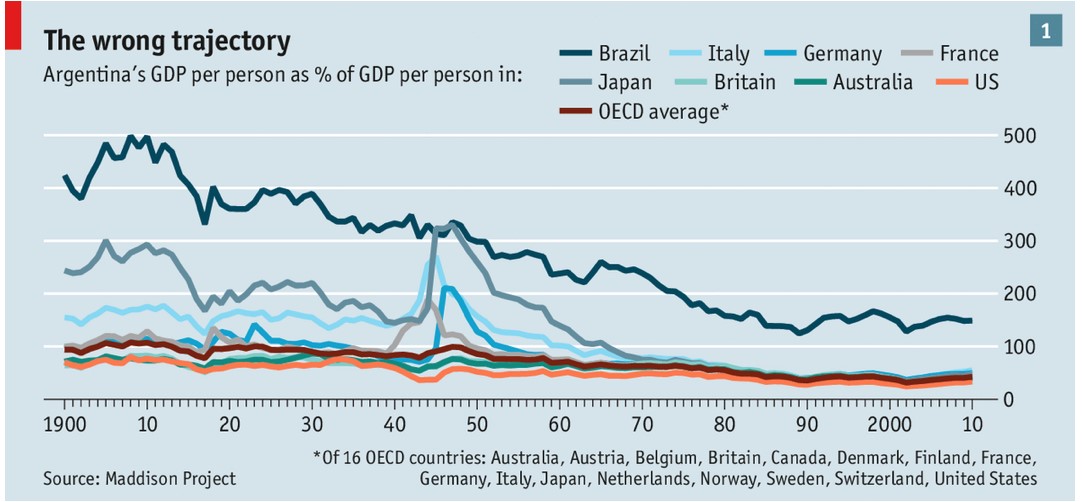

There’s almost no place that baffles economists more than Argentina. The South American nation began the 20th century among the wealthiest in the world, growing hugely prosperous from their commodities trade with Europe. Yet, since then, the nation has suffered a near constant decline. It is the lone wealthy nation from the turn of the 20th century that is not still comparatively wealthy today.

Source: The Economist

Source: The Economist

One big reason for Argentina’s decline is currency instability. Since 1973 alone, there have been three national currencies: the peso, the austral, and then a reconstituted peso. Poor fiscal policies have often stoked massive inflation that has placed serious downward pressure on Argentine currency. These currency depreciations in turn make foreign debt near impossible to repay, causing further devaluations which can ultimately result in economic collapse. Currency crises like this occurred in 1982 and 2001, and both have resulted in severe economic depressions.

Since Argentina’s mass currency depreciations have historically preceded economic crises, one wonders if perhaps changes in the value of the currency positively correlates with GDP growth—If the currency goes up, then does GDP also go up? This turns out to be a complicated question.

If you’re still reading at this point you must be an econ geek, and you might think, “But wait! Economic orthodoxy says that when the currency depreciates, GDP will increase. Cheaper currency means more competitive exports, which will boost output.” Exactly. This is what we want to test.

For some more recent historical context, Argentina over the past 10 years has continued to struggle with foreign debt and currency volatility. After the worst economic crisis in the nation’s history from 1998 to 2002, Argentina began to prosper again during the first few years of President Nestor Kirchner’s administration. Since the country defaulted on its debt in 2001, Argentina has had to borrow at relatively high interest rates. Adding to the mix, expensive government subsidies and other spending instituted under Kirchner and later his wife, President Cristina Kirchner, caused government debt to increase again around 2010. Since the 2015 election of President Mauricio Macri, the debt has only continued to increase. The US dollar has also strengthened as the Federal Reserve raises rates. As a result, Argentina’s dollar-denominated loans have become almost impossible to repay. Just months ago, the IMF stepped in and loaned Argentina $50 billion to help repay its most pressing debts. To make matters worse, the nation is currently in yet another severe recession.

All this raises the question: is there a positive relationship between changes in the country’s currency and GDP growth? Or does economic orthodoxy hold?

To answer this, we use daily currency data on the Argentine peso from the Central Bank of Argentina and data on GDP growth from the World Bank. We also use a common econometric technique designed to extract correlations between different variables while controlling for others—the ordinary least squares (OLS) regression, taught in all introductory econometric courses.

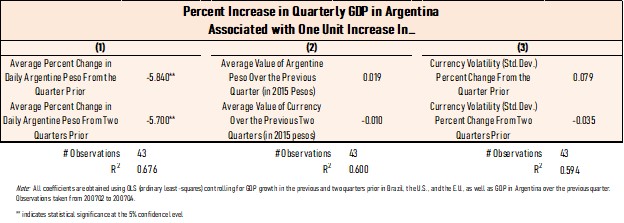

We first regress Argentine quarterly GDP growth from 2007 to 2017 on the average daily change in the Argentine peso during the two prior quarters. We also account for quarterly GDP growth in the United States, European Union, and Brazil during the same quarter, as well as GDP growth in Argentina, the US, EU and Brazil in the prior quarter. We find that the coefficients for the average change in the currency over the previous two quarters (quarters t−1 and t−2) are strongly negative, and statistically significant at the 5% level. This means that a one percent positive shift in the average daily change of the currency a few months prior is associated with a negative (approximately 1-9%) change in quarterly GDP growth.

This result is actually a bit misleading. If every day the Argentine peso appreciated by 1% for a whole quarter, then according to our model, GDP growth would be 1-9% lower than if the currency had stayed the same. That would be a massive change in GDP over one quarter. An average daily change of 1% in the currency value would mean the currency increased by roughly a factor of 2 over the entire quarter, but this never happened in any of the periods we observed. As far as the real world is concerned, smaller average daily changes in the value of the currency over the prior quarter (think maybe 0.2% at most) would indicate a roughly 0.2%-1.8% change in quarterly GDP growth in the following quarter. So we wouldn’t really expect Argentinian quarterly GDP growth to decline by more than 2% from an increase in currency value, since the currency can only fluctuate so much over a small period of time. Furthermore, this is only according to our model. As any statistician will always remind us, correlation is NOT causation.

If you found the prior paragraph a little too technical, it basically just says that an appreciation of the peso correlates with a decrease in GDP growth. This is just a correlation, and doesn’t mean for sure that an appreciation of the peso actually causes declines in GDP.

On the surface, the results appear to obey the logic of traditional economic theory. The old fashioned rules from textbooks say that an increase in currency should result in a negative change in GDP since exports become less competitive.

In reality, we should be cautious in rushing to conclusions. First, our data set involves 43 observations over a 10 year period. This period does not include the most recent IMF bailout in Argentina, which began in 2018. While Argentina was not macroeconomically stable over this time frame, the nation sustained average positive growth and avoided any catastrophic downturns like those of the 1980’s or early 2000’s.

Furthermore, our model does not account for two potentially important variables: inflation and net exports. Unfortunately, Argentina inflation statistics are notoriously inaccurate and have been subject to government meddling, especially under the Kirchner administrations. On top of that, inflation might be a “transmission mechanism”, a term economists use to describe a thing that affects another thing. So, when the currency falls, foreign goods become more expensive and inflation rises. This could cause the Argentine Central Bank to raise rates (since chronically high inflation is a recurrent problem) and thereby cause lowered GDP growth. Net exports is also a transmission mechanism since changes in the currency affect export and import levels and thus the overall economy. So while we didn’t account for inflation and net exports in our model, accounting for them may cause greater issues, since it would likely hide the true effect of currency changes on GDP growth by removing the process of how those changes affect GDP.

In an additional analysis, we regress Argentinian GDP growth on the average currency value during the two prior quarters. This is different from the average change in the currency since we are just using the actual currency value and not its change over time. All other model specifications are unchanged.

Interestingly, we find in this case that there is not a statistically significant relationship. Why? These results indicate that the actual value of the currency doesn’t seem to predict GDP growth. Rather, the change in the currency value is the statistically significant predictor. We wouldn’t necessarily expect a low valued Argentine peso to correspond with a rapidly growing economy unless the peso had declined in the two quarters prior.

So what does all this mean? Well, this provides clues that Argentina’s contemporary economy seems to obey the rules of the economic theory of exchange rates. When the currency goes down, growth seems to go up. It’s that simple. Despite all the talk of Argentina being the ultimate economic odd-man-out, perhaps it’s a bit more normal than everyone thought.

Featured Image Source: Frontera

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the UC Berkeley Economics Department and faculty, or the University of California at Berkeley in general.