NICOLAS DUSSAUX – MARCH 30TH, 2021

EDITOR: AMANDA ZHANG

Soon after the awarding of the Nobel Prize of Economics this year, a number of criticisms were levied against the Nobel committee’s decision. The decision to award the highest distinction in Economics to Stanford economists Paul Milgrom and Robert Wilson seemed to be disconnected to the current issues economics was supposed to address. These critics reignited an old debate about the role economics as a discipline is supposed to play in the world. Indeed, in the middle of the worst economic crisis since 2008, the choice to reward new designs for auctions with a Nobel Prize can seem only remotely related to the worries that kept economists busy this year.

To understand the reasoning behind this award, one has to understand that the work of Milgrom and Wilsen goes well beyond the basic sale of livestock or paintings that we instinctively think of when we think of auctions. The most basic definition of auction theory is: the science that studies what is sold, to whom and at what price. Many have already participated in an auction in their life, if not in person, then on eBay or another of the numerous websites that use auctions to allocate items. As it was outlined by the Royal Swedish Academy in their press release, auctions are a very old way to allocate items. However, what is new in modern-day auctions is the increasing complexity of the allocated items.

So, why use auctions, and what prompts the need for a deeper understanding of them?

The need to study auctions arises from the need to distribute goods to the right buyer. But, who is the right buyer? According to economic theory, the right buyer for an item is the buyer that most highly values that item. This allocation problem is usually solved by market mechanisms for goods where a large quantity is produced. However, for many goods, the pool of buyers is so narrow, and the number of items to allocate so small that we must come up with an alternate design to allocate them. Some of these items do not even have a cost of fabrication, making them very difficult to price. A non-exhaustive list includes oil wells, radio frequencies, and landing spots for planes, all of which have a very high social value and direct consequences on millions of people.

In an interview given to Stanford, Paul Milgrom advised prospective PhD Economics students to focus on real-life issues and challenges and proceed from there, rather than solving highly theoretical problems with no tangible applications. This was his thought process when he helped design the radio frequencies auctions with the Federal Communications Commission (FCC). Indeed, policy-makers realized that distributing licenses worth millions of dollars through the lottery made no economic sense and created many inefficiencies, as outlined by Milgrom in Putting Auction Theory to Work. The main problem induced by the former system of licensing was that the distribution of licenses was heavily influenced by the lobbying efforts of phone carriers that had to prove their project was the most socially beneficial to get a free license. Since the lottery system attracted speculators that drove up the prices of licenses, the system of auctions was therefore decided to be the best solution to allocate those licenses, but the hardest part of the problem was yet to be addressed: what design to adopt?

Auction theory allows us to address difficulties in the sale process that would have consequences for society at large. In the frequencies example, it was necessary for the bidders—the telephone companies—to be satisfied with the outcome of the bidding process and to be able to do business with the licenses purchased. The auction theorists that worked on the project rapidly realized that some of the licenses were not independent goods and that some licenses were complements or substitutes for others, therefore driving up their price when sold in a bundle. The theorists came up with a clever way to address this problem: instead of bidding on item after item, every license was sold at once, therefore excluding the risk of uninformed players bidding above value on the first licenses and destroying the additional value created by strategic bundles. More specifically, the bidding took place in rounds, with bidders placing their bets on sets of licenses, in an ascending auction, also known as an English auction. This design is called a Simultaneous Multi Round Auction (SMRA); it is a design in which Milgrom demonstrated that the ascending order of the bidding was better suited to avoid overpaying than a descending order (also called a Dutch auction). The risk of bidders sitting outside waiting to identify other bidder’s strategy was mitigated by implementing an activity rule that forced every bidder to place some bids at round n. Failure to do so results in the inability to place a significantly higher bid during round n+1. The auction of the radio frequencies was a bright success that put auction theory under the spotlight, and earned William Vickrey, the inventor of the field, a Nobel Prize in 1996.

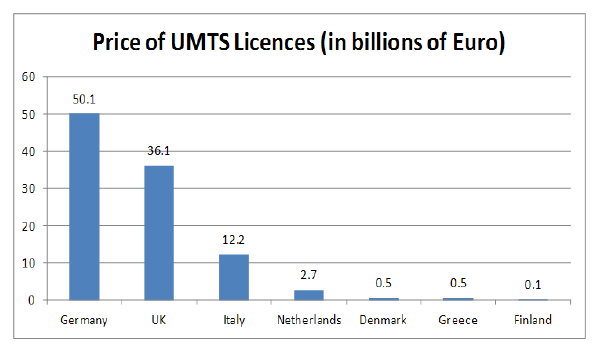

As it turns out, auctioning radio frequencies is a very lucrative way for governments to raise enormous revenues while ensuring that the markets behave in a correct way. As shown on the graph below based on McKinsey data, the amount of revenue generated by governments using new auctions design far exceeded the levels seen in countries that did not use them or neglected important design elements.

Image Source: “An Introduction to Auction Theory for Undergraduate students”, Felix Munoz-Garcia, 2012

Last month, a record auction allowed the US government to raise $81 billion over the allocation of frequencies for 5G carriers. The record-breaking revenue left the phone carriers with disproportionate debt, giving rise to one of the main concepts in auction theory: the winner’s curse—the risk for a bidder of spending so much on an item that they reap negative benefits. With no reliable way to estimate the revenue that the carriers can generate out of the 5G frequencies, there exists a significant risk that the bidders placed bids above their own valuation of the licenses, resulting in a deficit at best, and a threat of bankruptcy at worst. The largest phone carriers (T-Mobile, Verizon and AT&T) obviously kept in mind while bidding that failing to secure the right 5G frequencies would threaten their dominant position, pushing them to raise their bids. The design of the SMRA, meant to mitigate the risk of the winner’s curse, likely prevented a far worse outcome for both the phone carriers and the general public. However, companies overpaying for items is not supposed to be totally prevented by the auction design; rather, auctions were thought of as a way to split the total license revenue according to the relative willingness to pay of all bidders.

However, having the best design for an auction does not address the first criticism: why do we need to study auctions? Once the oil companies have their land, or the telephone carriers their frequency licenses, nothing keeps them from exchanging or reselling the items until each is attributed to a bidder that has the right valuation for it. This idea stems from the Coase Theorem, developed by the University of Chicago economist and Nobel Prize recipient Ronald Coase. In a free market, in the absence of barriers to transactions, and with perfect information, the bargaining process is supposed to yield an optimal outcome. However, this theorem is only a model, which fails to accurately predict real outcomes and overlooks the real-world barriers to trade and negotiation. The most common of all is the tendency for the buyer to underestimate the item and for the seller to artificially increase its value (to get the most surplus out of the transaction.) This problem cannot be overcome, as mechanism designers Myerson and Satterthwaite demonstrated in the 1990’s. This issue has direct implications on consumer welfare. If a phone carrier fails to purchase a license at an affordable yet fair price, it might end up in a position where it is unable to serve its customers well without charging them high prices. In the oil field example, trading drilling rights between companies imply very important imbalances in information, therefore creating risk for both parties and heavy transactional costs.

Designing efficient resource allocation mechanisms is important for consumer welfare, but the insights brought by auction theory are also useful in environmental economics. Besides the very famous use of auctions to set clearing prices in the electricity markets, climate finance also uses auction theory to enhance carbon reduction. In early March 2020, at the peak of the Covid-19 crisis, 21 companies took part in an online auction to buy the right to sell carbon credits in the future. The options were sold in a descending auction, the decreasing price allowing to weed out companies for which the costs of abatement would not be covered by the funds of the World Bank. The design allowed the World Bank to achieve a sale of $8.25 million of credits to the most performing companies in the matter, which could lead to an emission reduction of 4.2 million tons of carbon dioxide by the end of 2020.

As the economist Noah Smith outlined in a recent article for Bloomberg, economists increasingly resemble engineers in their way of thinking and in the direct usefulness of their work. A lot of economic theories are attempts to explain what happens in markets with a broad set of unrealistic assumptions. This work is crucial, but it often takes a lot of steps to go from theory to the elaboration of clever public policies, and even more to go from there to implementation. Contrarily, auction theory allows economists to create tools for governments, international organizations and private companies, such as engineers would do, in a manner that does not involve politics and increases efficiency. In the case of auction theory, getting the allocation of resources and goods right is an essential part of establishing fairer and more efficient economic systems, which the Nobel Prize committee rightly acknowledged. Perhaps Paul Milgrom and Robert Wilson were not so disconnected from the real world after all?

Featured Image Source: Economic Confidential

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the Undergraduate Economics Association, the UC Berkeley Economics Department and faculty, or the University of California, Berkeley in general.